Over the last few months, we’ve explored the mechanics of wealth: from the psychological momentum of debt paydown to the tax-efficient structures of S-Corps and the relentless power of compounding. But knowledge without a system is just noise. To achieve true financial freedom in 2026, you need a Blueprint.

This final post is your step-by-step roadmap to integrating the Cortex ecosystem into your daily life. Here is how to move from “financial stress” to “total clarity” in exactly six months.

Month 1: The Diagnostic Phase

You cannot improve what you do not measure. Your first 30 days are about establishing your baseline. Stop looking at your bank balance and start looking at your Trajectory.

- Week 1: Audit your assets and liabilities. Establish your “North Star” number.

- Week 2: Implement the Anti-Budget. Identify your “Tension Metrics” and give yourself permission to spend guilt-free on what matters.

- Featured Tool: Net Worth Engine

Month 2: The Efficiency Scrub

Month 2 is about plugging the leaks. We’re looking for “lazy cash” and unoptimized debt that is dragging down your momentum.

- The Scrub: Perform your 48-hour Financial Hygiene audit. Cancel zombie subscriptions and move cash to high-yield accounts.

- The Pivot: Use the Hybrid Debt Strategy to knock out a small win and then attack high-interest rates.

- Featured Tool: Debt Paydown Strategy Optimizer

Month 3: The Big Ticket Optimization

Now that the small leaks are plugged, we address the “Big Three”: Housing, Transportation, and Location. This is where the largest gains are made.

- The Car Check: Apply the 20/3/8 Rule to your current vehicle. If you’re “car poor,” make a plan to downsize.

- The Reality Engine: Run the numbers on your home. Is it an asset or an anchor? Explore Geographic Arbitrage to see if a change of zip code could save you $1M.

- Featured Tool: Rent vs Buy Reality Engine

Month 4: The Wealth Accumulation Engine

With your expenses optimized and your debt shrinking, it’s time to turn on the growth engine. This month is about Ownership.

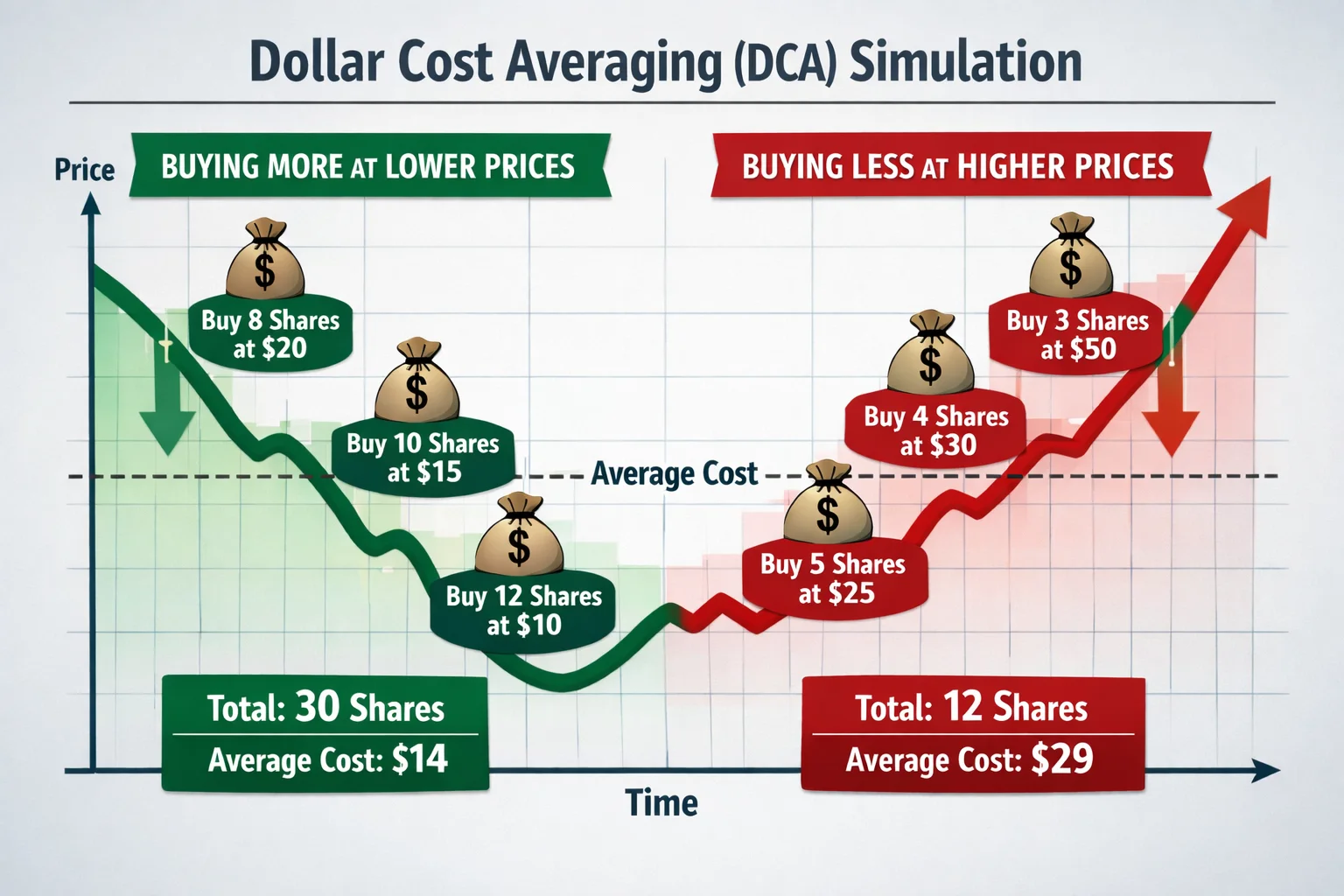

- Core Investing: Choose your core index funds (VOO vs. QQQM) and automate your contributions.

- The Redirect: Take the money saved from your efficiency scrub and the “odds” you used to play, and funnel it into the market.

- Featured Tool: Index Fund Growth Visualizer

Month 5: The Entrepreneur’s Edge (Optional)

If you own a business or freelance, Month 5 is your tax-savings masterclass. If you don’t, use this month to double down on your career Mobility Premium.

- S-Corp Check: Find your “Reasonable Salary” and calculate your self-employment tax savings.

- Retirement Maxing: Split your contributions between Employer and Employee portions to shield the maximum amount of income from the IRS.

- Featured Tool: S-Corp Tax Optimizer

Month 6: The Exit Strategy

In the final month, we look at the finish line. Whether retirement is 5 years or 25 years away, you need to know how the “End Game” works.

- Stress Testing: Run your portfolio through Sequence of Returns simulations.

- RMD Planning: Map out your future tax obligations to ensure the IRS doesn’t eat your hard-earned 401(k).

- Featured Tool: Retirement Strategy Engine

Your Journey Begins with One Number

The 6-month blueprint only works if you take the first step. Financial clarity isn’t a destination; it’s a system of hygiene and optimization that builds over time.

Start today by identifying your baseline. Use the Cortex Net Worth Engine to visualize your current trajectory and see exactly where the next six months can take you.